AI tools are transforming retirement withdrawal planning by offering tailored strategies that help retirees make smarter financial decisions. These tools analyze your full financial picture, adjust for market changes, and provide clear guidance on optimizing withdrawals. Key benefits include:

- Tax efficiency: AI minimizes tax burdens by recommending optimal withdrawal sequences (e.g., taxable accounts first, then tax-deferred, and finally Roth accounts).

- Dynamic adjustments: AI tools monitor portfolios in real-time, suggesting changes based on market conditions and personal needs.

- Simplified guidance: Natural language models explain complex financial concepts in plain terms, making decisions easier to understand.

- Scenario simulations: Tools like Monte Carlo simulations predict how different strategies perform under various conditions, offering clarity on risks and outcomes.

Platforms like Mezzi lead the charge by consolidating financial accounts, automating tax strategies, and offering cost-effective solutions. While AI excels in data analysis and strategy, human advisors remain vital for emotional support and handling complex scenarios. Combining AI with expert advice ensures a more secure and informed retirement plan.

Using AI for Tax-efficient Withdrawal Strategy after Retirement

Key AI Technologies in Retirement Withdrawal Optimization

AI-powered tools are reshaping how retirees manage their finances by offering personalized strategies for withdrawing funds. These tools go beyond basic calculators, leveraging advanced algorithms to analyze detailed financial scenarios and deliver tailored recommendations. With features like real-time adjustments, in-depth simulations, and user-friendly guidance, AI is redefining retirement planning.

Dynamic Portfolio Adjustments Using AI

AI excels at creating withdrawal strategies that adapt to your financial needs and changing market conditions. Unlike static withdrawal rules, these systems continuously monitor your portfolio and make recommendations based on shifts in the market and your personal circumstances.

For example, machine learning models can evaluate your risk tolerance and suggest annuity options that align with your financial goals and behavior. These tools account for a variety of life events, such as rising healthcare costs or legacy planning, ensuring your strategy evolves as your needs change. A practical example of this is TIAA's use of AI to assess risk tolerance and recommend annuity options, showcasing the real-world benefits of this technology.

"AI should be viewed as a tool to complement actuarial expertise and support retirees in achieving their financial goals in retirement." - Elizabeth Walsh, FSA, MAAA, Vice President and Actuary at TIAA

AI-driven robo-advisors take this a step further by building diversified portfolios tailored to your financial goals, risk tolerance, and investment timeline. They identify potential risks and adjust strategies to protect against losses, ensuring a steady income stream. These systems also recommend asset allocations that match your risk appetite and investment objectives.

In addition to these dynamic adjustments, AI enhances risk analysis through detailed simulations, offering deeper insights into potential outcomes.

Scenario Simulations and Stress Testing

AI brings a new level of sophistication to retirement planning with tools like Monte Carlo simulations. These simulations explore a wide range of possible outcomes by factoring in market volatility, helping you see how your strategy might perform under different conditions.

By automating scenario generation and analyzing complex market data, AI can uncover relationships and risks that traditional models might miss. For instance, AI algorithms can model interactions between asset classes, sectors, and global markets, providing a more comprehensive view of vulnerabilities.

Agent-based simulations take this further by mimicking the behavior of market participants during stress conditions. These tools assign probabilities to different scenarios, helping you prioritize risks and allocate resources effectively. They also generate forecasts based on your spending habits, inflation trends, and potential healthcare costs, giving you a clearer picture of your financial future.

"A stress test is an exercise to see how the portfolio withstands different market outcomes." - Cassandra Rupp, Senior Wealth Advisor and Certified Financial Planner at Vanguard

Financial advisors often aim for a probability of success score of 85% or higher in these simulations. A Monte Carlo score of 75, for example, indicates a 75% likelihood of meeting your retirement goals. By incorporating real-time market data, AI improves the accuracy of these forecasts, offering more reliable guidance for your withdrawal decisions.

Natural Language Models for User-Friendly Guidance

AI doesn’t just crunch numbers; it also makes complex financial concepts easier to understand. Natural language processing (NLP) plays a key role in simplifying sophisticated analysis for retirees. These systems translate technical jargon into clear, actionable advice that’s easy to follow.

For example, AI-powered platforms can create personalized educational materials to help you make informed decisions about retirement planning. Instead of overwhelming you with complex terminology, they explain why specific strategies are recommended and how they align with your goals.

NLP tools also provide tailored explanations based on your financial knowledge and circumstances. They can clarify tax implications, explain portfolio adjustments, and show how different withdrawal sequences impact your long-term financial security. Additionally, conversational interfaces allow you to ask questions about your retirement plan and receive immediate, personalized responses in plain English.

Research Insights: How Well AI-Driven Tools Work

Recent studies highlight how AI-powered tools can provide measurable benefits, such as crafting personalized strategies, while still grappling with certain limitations. These findings offer a foundation to explore both the strengths and challenges of these tools.

Better Portfolio Longevity and Tax Efficiency

AI tools have shown promise in improving portfolio longevity and reducing tax burdens by optimizing withdrawal strategies. By analyzing an individual's complete financial profile, these systems can tailor recommendations to specific needs. Their ability to process large amounts of data allows them to identify market trends and offer predictive insights for timing and structuring withdrawals. Research also suggests that retirees benefit from these tools when selecting financial products that align with their goals, whether it's ensuring steady income, planning for legacy, or addressing inflation risks. Additionally, these tools consider various life events - such as education costs, healthcare needs, and inheritance planning - providing a comprehensive approach to long-term financial management.

Adjusting to Life Events

AI tools stand out for their ability to adapt to major life changes. When unexpected expenses or significant events occur, these systems can quickly reassess financial plans, recalibrating withdrawal strategies to align with the new circumstances. For instance, they evaluate how such changes affect long-term financial stability and adjust recommendations on annuities or withdrawal rates accordingly. These tools are also skilled at tailoring advice to different demographics, offering personalized recommendations that reflect individual goals, challenges, and values.

Limitations and Data Requirements

Despite their advantages, AI-driven tools come with notable limitations. Errors can arise due to data or algorithm shortcomings, and these systems may struggle with highly complex scenarios. For example, AI often falls short in handling intricate tax strategies, estate planning, or long-term care costs, areas that typically require human expertise. Another significant drawback is the lack of emotional intelligence - AI cannot provide the reassurance or strategic guidance needed during market downturns or stressful life events.

Data privacy is another concern, as these tools require extensive access to personal financial information to function effectively. Additionally, the absence of human interaction can be a disadvantage during emotionally charged financial decisions. As Jason Gilbert, founder and managing partner of RGA Investment Advisors, points out:

"AI lacks the judgment, intuition and forward-looking perspective that come from decades of experience."

Overreliance on AI can lead to missed opportunities, unforeseen tax liabilities, and inadequate financial preparation. This is particularly concerning given that 75% of workers report financial worries at work, impacting productivity, while 47% say their finances are a source of stress.

Research underscores that AI works best as a complement to human financial expertise. As Ryan McLin, founder and lead financial advisor at Impact Wealth Group, explains:

"When used effectively, it enhances the client experience by improving efficiency and allowing the advisor to focus on providing expert guidance, but the relationship between a client and their advisor remains irreplaceable."

To maximize the benefits of AI tools, financial professionals recommend cross-checking AI-generated advice with a qualified expert and ensuring that recommendations align with individual goals and circumstances.

Mezzi: AI-Powered Platform for Tax-Efficient Withdrawals

Mezzi is reshaping tax-efficient withdrawal planning by using AI to deliver personalized strategies. It aims to make advanced tax optimization accessible to everyone, moving away from the traditionally high costs of financial advisors.

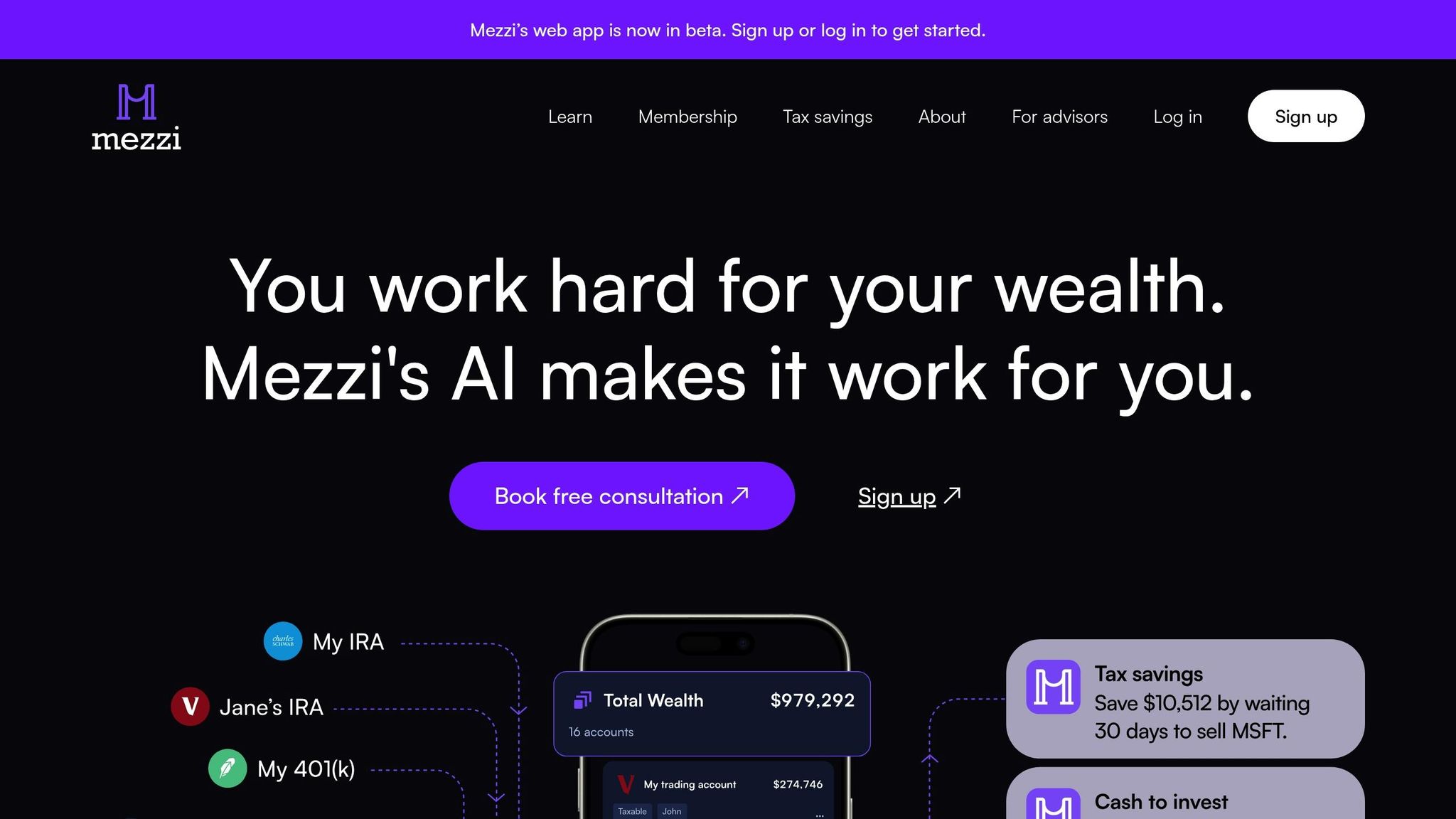

All-in-One Financial Account Dashboard

Mezzi consolidates all your financial accounts into a single, easy-to-navigate dashboard. From taxable investment accounts to tax-deferred options like 401(k)s and traditional IRAs, and even tax-exempt Roth accounts, everything is in one place. This means you can view your entire financial situation at a glance or dive into specific accounts without juggling multiple logins.

This comprehensive view is crucial for smart retirement withdrawal planning. Without it, many investors unknowingly make less-than-ideal choices. For instance, withdrawing from a Roth IRA might seem convenient but could be less tax-efficient compared to tapping into a traditional IRA, depending on your current income bracket. By providing a full financial picture, Mezzi helps users make better-informed decisions.

To ensure secure data connections, Mezzi relies on trusted aggregators like Plaid and Finicity. These tools not only safeguard privacy but also make it easier for users to link their accounts. With this unified approach, the platform identifies opportunities and potential risks across the board, turning users into proactive decision-makers guided by AI-powered recommendations.

Smart Tax Optimization Tools

Mezzi doesn’t stop at account aggregation - it takes tax optimization to the next level. One standout feature is its ability to prevent wash sale violations across all accounts, a common challenge for active investors managing multiple portfolios. This ensures compliance with tax rules while avoiding unnecessary penalties.

The platform also provides tailored withdrawal strategies. For example, it might suggest starting with taxable accounts, followed by tax-deferred accounts, and finally Roth accounts to maximize tax-free growth. Other advanced features include identifying tax-loss harvesting opportunities and recommending Roth conversions during low-income years to reduce future tax burdens.

Another highlight is Mezzi’s X-Ray feature, which detects hidden stock exposures across accounts. This helps users avoid accidentally concentrating too much of their portfolio in similar investments, a risk many overlook when managing multiple accounts or fund families.

These tools don’t just optimize taxes - they save both time and money by simplifying complex strategies that would otherwise require costly professional advice.

Savings and Convenience for Users

Mezzi offers substantial benefits, including significant cost savings and time efficiency. By reducing or eliminating the need for financial advisors, users could save upwards of $1 million over 30 years. The platform also automates intricate tax strategies, freeing up time for other priorities.

With instant AI-driven insights, users can quickly make informed decisions, a major advantage for active investors who frequently adjust their portfolios or withdrawal plans based on market changes.

Mezzi provides two access levels: a free version and a $199 annual Premium Membership. The free version includes basic tools like consolidated account views and family collaboration features. The Premium Membership unlocks advanced capabilities, such as real-time AI insights, unlimited AI chat, and detailed tax and fee savings analysis.

By focusing on AI’s strengths - like data processing, pattern recognition, and compliance with tax rules - Mezzi enhances, rather than replaces, human judgment. Its conversational AI interface simplifies complex retirement decisions, boosting user confidence and engagement.

To address concerns about data security, Mezzi employs robust measures, including end-to-end encryption and multi-factor authentication. These protections ensure that sensitive financial information stays secure throughout the analysis process, addressing a common worry with AI-based financial tools.

sbb-itb-e429e5c

Conclusion: The Future of AI in Retirement Planning

AI is reshaping how Americans approach retirement withdrawal planning, turning what was once an exclusive service into technology accessible to everyone. Research shows that AI became mainstream in 2023, significantly influencing financial planning practices.

Key Takeaways

AI-powered withdrawal tools offer more than just convenience - they deliver measurable benefits. These platforms analyze countless variables to craft personalized strategies that adapt to market changes and individual circumstances. For self-directed investors, these tools provide tax optimization, dynamic asset allocation, and risk management - services that were once the domain of high-cost advisors.

One of the standout advantages is tax efficiency. AI systems can spot tax-loss harvesting opportunities, avoid costly wash sale violations across multiple accounts, and recommend withdrawal sequences that minimize tax burdens. Platforms like Mezzi excel in optimizing taxes and reducing fees, leading to substantial long-term savings.

Another game-changer is flexibility and personalization. Unlike static rules, AI evolves with spending habits, market trends, and personal situations. These systems can even incorporate health data, family history, and lifestyle factors to create more accurate longevity estimates, ensuring withdrawal strategies align with real-life needs.

The democratization of financial advice is bridging a critical gap in retirement planning. With only 35% of Americans having a financial plan and 82% of Europeans reporting low or medium financial literacy levels, AI-integrated tools are helping retirees gain better financial security. This shift is especially evident as more retirees favor advisors who use AI to enhance their services.

"The promise of artificial intelligence is in its capacity to reduce complexity... This enables people to be more confident and wiser in their choices."

- Arjun Bali, Senior Data Scientist at Rocket Mortgage

These advancements set the stage for a future where AI continues to evolve to meet the diverse needs of retirement planning.

Looking Ahead: AI's Expanding Role

The next decade promises even more advanced AI capabilities in retirement planning. Real-time forecasting engines will deliver continuously updated projections, while improved natural language models will make complex financial concepts easier to understand. AI's ability to adapt to personal needs and market changes will only strengthen over time.

Hyper-personalization will be a major focus. Future AI systems will analyze financial data alongside behavioral patterns, life goals, and personal values to create deeply individualized strategies. This could include identifying alternative investments and asset classes that align with a person’s risk tolerance and retirement timeline.

Integration with workplace retirement plans is also gaining momentum. Surveys reveal that 52% of plan sponsors believe AI will help workers choose investments tailored to their goals, while 49% expect AI to create customized retirement strategies. This is crucial, given that 60% of retirement plan participants feel overwhelmed by plan details, and 77% want more professional guidance.

AI is also addressing longevity challenges as Americans live longer. Advanced algorithms now factor in extended retirement periods and evolving healthcare needs, ensuring portfolios are designed to last throughout retirement.

"Technology is only as good as the intention and ethics behind it. If these tools are built with transparency, fairness, and human well-being in mind, they can absolutely help people make smarter, more informed choices about their retirement. The key is to make sure AI is used to empower, not overwhelm or manipulate."

- Faisal Hoque, Technologist and Author

Despite these advancements, human insight remains irreplaceable. As Jeff Sippel, Chief Strategy Officer at Northwestern Mutual, explains:

"Financial planning isn't just about numbers on a spreadsheet – it's an emotional discussion around a person's life goals. These conversations are complex, delicate and deeply personal. Clients want to discuss their options with a trusted financial advisor who understands their needs and the trade-offs associated with these big financial decisions at a human level."

For self-directed investors, the takeaway is clear: integrating AI tools into retirement planning can help safeguard against financial uncertainties. Platforms like Mezzi are leading the charge, making sophisticated financial insights accessible to anyone ready to take control of their retirement. The future belongs to those who embrace these tools while staying actively involved in their financial decisions.

FAQs

How can AI tools help optimize taxes during retirement withdrawals?

How AI Tools Help Optimize Taxes in Retirement

AI tools can make a big difference when it comes to managing taxes during retirement. By evaluating your entire financial picture, they craft personalized withdrawal strategies that aim to reduce tax burdens. For example, they analyze the best timing and order for pulling money from various accounts - like traditional IRAs, Roth IRAs, and taxable accounts.

What’s more, these tools stay updated with changes in tax laws and shifts in your personal circumstances. This means they can provide real-time guidance to help you maintain tax efficiency over the long haul. The result? Retirees get to hold on to more of their savings, ensuring a stronger financial foundation for the years ahead.

How do human advisors complement AI tools in retirement withdrawal planning?

The Role of Human Advisors in Retirement Planning

Human advisors bring something to the table that AI tools simply can’t replicate: a personal touch. They offer guidance tailored to your specific financial circumstances, help you untangle tricky legal and tax matters, and provide the emotional reassurance that no algorithm can deliver.

While AI excels at crunching numbers and delivering custom recommendations, human advisors take it a step further. They review AI-generated insights to verify accuracy, spot any biases, and craft strategies that are comprehensive and well-balanced. Their expertise ensures your financial plan stays on track with your long-term goals, leaving you with a sense of clarity and confidence.

How do AI tools adjust retirement plans to fit changing personal and market conditions?

AI tools work behind the scenes, constantly processing real-time data to fine-tune retirement strategies as your life circumstances and market conditions shift. Whether it's an income change, market swings, or a shift in your financial priorities, these tools adjust investment allocations and withdrawal plans accordingly.

This ongoing adaptability helps keep your retirement plan on track, balancing risks while aligning with your evolving needs to support better long-term results.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.