When comparing BND and AGG, two top bond ETFs, the main differences are in their expense ratios, liquidity, and tracking methods. Both offer broad exposure to the U.S. bond market, with similar credit quality and duration profiles, but slight nuances can influence their performance depending on your investment style.

Key Points:

- Expense Ratios: BND has a slightly lower expense ratio, which can benefit long-term investors.

- Liquidity: AGG sees higher trading volume, making it better for frequent traders or large portfolios due to tighter bid-ask spreads.

- Tracking Methods: BND uses full replication for broader market representation, while AGG employs sampling for enhanced liquidity during volatile periods.

- Performance in Rate Cycles: Both funds react similarly to rate changes, with price drops during rising rates and gains when rates fall.

- Credit Quality: Both focus on investment-grade bonds, with heavy allocations to U.S. Treasuries, agency bonds, and high-quality corporate debt.

Quick Comparison:

| Feature | BND | AGG |

|---|---|---|

| Expense Ratio | Lower | Slightly higher |

| Liquidity | Lower trading volume | Higher trading volume |

| Tracking Method | Full replication | Sampling |

| Credit Quality | Similar (AAA, AA, A, BBB) | Similar (AAA, AA, A, BBB) |

| Rate Sensitivity | Comparable duration profiles | Comparable duration profiles |

| Best For | Long-term, buy-and-hold investors | Active traders, larger portfolios |

Conclusion:

Choose BND if you're focused on minimizing costs for long-term investing. Opt for AGG if you prioritize liquidity and smoother trade execution, especially in volatile markets. Both are strong core bond holdings, so your choice depends on your trading habits and portfolio size.

BND vs. AGG - Which Total U.S. Bond Market Fund?

Fund Structure and Basic Differences

To understand why BND and AGG might perform differently, it's essential to look at how they're structured. While both aim to replicate the U.S. bond market, differences in fees, trading activity, and how they track their benchmarks can influence their outcomes. These foundational distinctions pave the way for a closer look at risk and performance metrics later on.

Expense Ratios and Annual Costs

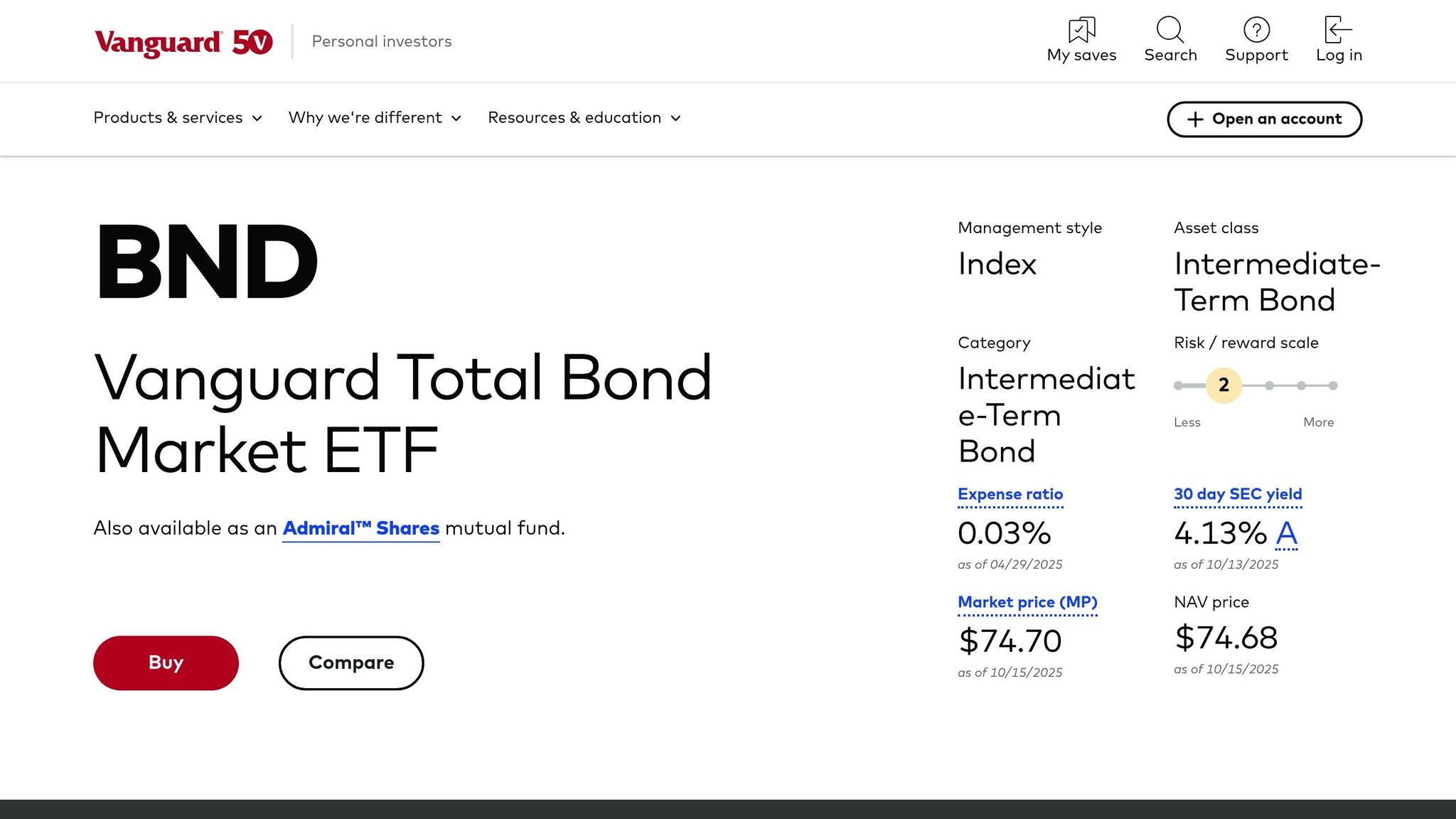

BND tends to have a slightly lower expense ratio compared to AGG. Even minor differences in annual fees can add up significantly over time, potentially boosting long-term returns. This is especially important for investors with a large portion of their portfolio allocated to bonds, as lower costs can have a noticeable impact on overall performance.

Trading Volume and Fund Size

AGG generally experiences higher daily trading volumes, thanks to its longer market history and popularity with institutional investors. BND, on the other hand, sees comparatively lower trading activity. Additionally, AGG manages a larger asset base, which can lead to tighter bid-ask spreads under typical market conditions. For frequent traders or those making regular portfolio adjustments, AGG's higher liquidity can be advantageous. However, for buy-and-hold investors, these differences are less critical.

Holdings Count and Index Tracking Methods

BND uses full replication to closely mirror its benchmark, holding a wide array of bonds. AGG, however, employs a sampling method, which prioritizes liquidity while still achieving minimal tracking error. During periods of market volatility, sampling can enhance liquidity, while full replication ensures a broader representation of the bond market. Despite these differences, both funds effectively deliver the expected exposure to the U.S. bond market with minimal deviation from their respective benchmarks.

Duration and Interest Rate Risk

When it comes to understanding how bond funds react to changes in interest rates, duration plays a critical role. It essentially measures how sensitive a bond fund's price is to rate adjustments. By grasping the concept of duration, investors can better anticipate how bond prices might shift when interest rates move. Both BND and AGG are subject to duration risk, though the way their portfolios are constructed can lead to slight differences in how they respond. These nuances in duration set the stage for comparing how each fund handles changes in interest rates.

What Duration Means for Bond Investors

Duration represents how much a bond fund's price might change in response to a one-percentage-point move in interest rates. For instance, if a fund has a duration of six years, a 1% increase in rates could lead to an approximate 6% drop in the fund's price. Conversely, if rates fall by 1%, the price might rise by about 6%. This inverse relationship between rates and bond prices is a fundamental principle of bond investing. Effective duration goes a step further, accounting for factors like callable bonds, to provide a more refined estimate of sensitivity.

Duration Numbers: Current and Historical Data

Historically, both BND and AGG have maintained similar effective duration profiles. While differences in their methodologies - such as full replication versus sampling - can slightly alter the average maturity of their holdings, their overall sensitivity to interest rate changes has remained consistent over time.

Rate Change Examples and Price Impact

Looking at past interest rate cycles helps illustrate how duration impacts bond fund performance. In periods of rising rates, funds with higher effective durations tend to experience sharper price declines. Conversely, when rates fall, these same funds often see their prices climb as bond values adjust upward. To estimate the potential impact, investors can multiply the expected rate change by the fund's duration. However, it’s essential to remember that actual results may vary due to other market dynamics and income contributions, which also play a role in total returns. This understanding provides a solid foundation for evaluating how each fund performs across different rate environments.

Credit Quality and Bond Types

The credit composition of a bond fund directly impacts its risk and income potential. For investors, understanding how BND and AGG allocate their holdings across various credit qualities is key to determining which fund aligns better with their risk tolerance and income goals. While both funds emphasize investment-grade bonds, their specific allocations to government securities, agencies, and corporate bonds create subtle but meaningful differences in their risk profiles. Let’s dive into the credit ratings within each fund to better understand these distinctions.

Credit Rating Breakdown by Percentage

Both BND and AGG concentrate on investment-grade bonds, with AAA-rated securities taking up the largest share in each fund. This is largely due to their heavy holdings in Treasury and agency bonds, which prioritize safety over yield. These securities are considered some of the safest investments available, though they typically offer lower yields compared to bonds with lower credit ratings.

AA and A-rated bonds strike a balance between safety and income, offering slightly higher yields while maintaining a low risk of default. These bonds are often composed of high-quality corporate debt and select government agency securities.

BBB-rated bonds, which sit at the lower end of the investment-grade spectrum, make up a smaller portion of both funds. While these bonds carry a slightly higher risk of default, they also provide the potential for enhanced yields. The similar distribution of credit ratings between BND and AGG underscores their shared goal of offering broad exposure to the U.S. bond market.

From credit ratings, let’s shift focus to government and agency bond exposure, a critical factor in each fund's risk profile.

Government Bond and Agency Exposure

Both funds rely heavily on U.S. Treasury securities, which form the foundation of their portfolios. Treasuries are backed by the full faith and credit of the U.S. government, making them one of the most secure investments available. These holdings include a mix of Treasury bills, notes, and bonds with varying maturities, offering stability and liquidity to BND and AGG alike.

Government agency bonds are another important component. These include securities issued by organizations like Fannie Mae and Freddie Mac. While they lack explicit government guarantees, they are widely perceived as having implied government backing, placing them just a step below Treasuries in terms of credit quality.

Mortgage-backed securities (MBS) issued by government agencies also play a significant role in both funds. Backed by pools of residential mortgages, these securities provide diversification and slightly higher yields compared to Treasuries. This exposure allows both BND and AGG to tap into the mortgage market while maintaining their high credit quality standards.

Corporate Bond Allocation

Corporate bonds serve as another critical layer of income and risk in both funds. Investment-grade corporate bonds are a key source of yield, offering returns higher than government bonds to compensate for additional credit risk. These bonds are issued by well-established companies with strong credit ratings, ensuring a conservative approach to risk management.

The corporate bond exposure in both BND and AGG spans various sectors, including financials, industrials, utilities, and technology. This sector diversification reduces concentration risk and provides exposure to a broad range of industries. For instance, financial sector bonds often comprise a significant portion due to the large issuance volumes from banks and insurance companies.

Utility bonds contribute stable and predictable income, while industrial bonds offer exposure to a wide range of manufacturing and service companies. Together, these corporate allocations enhance the yield of both funds without venturing into the riskier territory of high-yield or "junk" bonds. By focusing exclusively on investment-grade corporate debt, both BND and AGG maintain their conservative risk profiles while still delivering meaningful income potential beyond what government bonds alone can provide.

sbb-itb-e429e5c

Performance During Different Rate Cycles

When it comes to investing in bond funds, understanding how they behave in different interest rate environments is key. Both BND and AGG have navigated through various rate cycles since their inception, offering valuable lessons about their performance during market turbulence and periods of opportunity. Their patterns often mirror shifts in Federal Reserve policies and broader economic changes.

Rising Rate Periods: 2013, 2016–2018, and 2022–2023

Rising rates have historically posed challenges for both funds. During the 2013 Taper Tantrum, market expectations around Federal Reserve policy shifted abruptly, leading to declines in both funds.

From 2016 to 2018, the Federal Reserve executed a gradual series of rate hikes. While the steady pace of increases created headwinds, income from coupon payments helped offset some of the impact. These years highlight the funds' sensitivity to rising rates and their ability to recover as conditions stabilize.

The 2022–2023 period brought a much faster pace of rate hikes, creating significant challenges. The Federal Reserve’s aggressive tightening of monetary policy led to sharp downturns for both funds, emphasizing their vulnerability in an environment of rapid rate increases.

Falling Rate Periods: 2019 and 2020

When rates fall, bond funds typically benefit, and both BND and AGG followed this trend. In 2019, as the Federal Reserve began cutting rates, both funds posted strong positive returns.

The 2020 pandemic brought an even more dramatic response, with swift rate cuts and quantitative easing fueling gains for both funds. However, as older, higher-yielding bonds matured and were replaced by new, lower-yielding ones, dividend distributions adjusted to reflect the changing portfolio composition.

Stable Rate Periods and Income Generation

In periods of relatively stable interest rates, the focus shifts to generating income. During these times, BND and AGG have consistently provided reliable monthly income distributions, thanks to steady portfolio management and alignment with their benchmarks. This stability makes them appealing choices for investors looking for predictable cash flows.

Trading Costs and Portfolio Implementation

When evaluating funds, it's not just about performance metrics - trading execution and tax implications play a big role in how a portfolio operates in the real world. Trading costs and management strategies directly affect returns, so understanding these factors can help you choose the fund that aligns best with your goals.

Bid-Ask Spreads and Trading Costs

Both AGG and BND are known for their strong liquidity, but AGG has a slight edge when it comes to trading efficiency. AGG averages 8,037,780 daily shares traded, compared to BND's 6,547,603. This higher trading volume often leads to narrower bid-ask spreads, which can reduce the cost of executing trades.

"AGG tends to have higher trading volume and liquidity compared to BND, which can result in narrower bid/ask spreads and potentially better execution for investors." – etf.com

For most investors, these differences in trading costs are relatively small. However, if you're someone who trades frequently or deals with large orders - especially in volatile markets where spreads can widen - AGG's superior liquidity might offer better execution and lower costs. These factors are especially important when considering tax implications and portfolio turnover.

Tax Efficiency and Portfolio Turnover

Both AGG and BND generate taxable income, with portfolio turnover occasionally resulting in small capital gains. Interest payments from these funds are taxed as ordinary income, not as qualified dividends, which can impact after-tax returns. Additionally, the routine buying and selling of bonds to maintain target durations can lead to minor recurring capital gains distributions. These tax and turnover factors are worth considering, particularly if you're focused on after-tax performance.

Portfolio Size and Trading Frequency Considerations

For long-term, buy-and-hold investors, the differences in trading costs and liquidity between AGG and BND are unlikely to have a significant impact on overall returns. However, for active traders or investors managing larger positions, AGG's higher liquidity can make a noticeable difference over time. In tax-advantaged accounts, where tax considerations are less of a concern, the emphasis shifts to trading execution and minimizing overall costs.

Final Comparison and Selection Guide

BND and AGG are two core bond funds with much in common, but their subtle differences can influence your investment decisions. Let’s break down these distinctions to help you decide which fund aligns better with your trading habits and portfolio needs.

Key Differences at a Glance

AGG stands out for its higher liquidity, which translates to tighter bid-ask spreads. Meanwhile, both funds share nearly identical duration and credit quality profiles, as they track broad U.S. bond market indexes that include government, agency, and corporate bonds.

When it comes to historical performance, the two funds have been similarly reliable across various interest rate environments - whether rates are rising, falling, or holding steady. This consistency highlights their strength as dependable core bond investments.

Choosing Between BND and AGG

Your choice between these funds largely depends on your trading style and the size of your portfolio:

- For Active Traders: If you trade frequently or manage larger positions, AGG’s superior liquidity can result in smoother execution and lower transaction costs, especially during volatile markets.

- For Long-Term Investors: If you’re a buy-and-hold investor focused on retirement savings or building long-term wealth, either fund works well as a foundational bond holding.

- For Different Portfolio Sizes: Larger portfolios may benefit from AGG’s liquidity, which can enhance trade efficiency. For smaller portfolios, the difference in liquidity is less likely to have a noticeable impact.

Final Thoughts

Both BND and AGG offer broad exposure to the U.S. bond market and deliver comparable performance across interest rate cycles. The decision comes down to how well each fund fits into your overall investment strategy. AGG’s liquidity may appeal to active traders, while long-term investors can confidently choose either option without worrying about significant performance differences. Consider your trading frequency and portfolio size to pick the fund that best complements your financial goals.

FAQs

How do BND and AGG's expense ratios affect long-term returns?

Both BND (Vanguard Total Bond Market ETF) and AGG (iShares Core U.S. Aggregate Bond ETF) stand out for their incredibly low expense ratios of just 0.03%. This makes them some of the most cost-effective options for investors. With fees this low, more of your money remains invested in the fund, which can have a big impact on your returns over the long haul - especially when compounded.

For fixed-income investors, keeping costs down is essential. Bond returns tend to be more modest compared to stocks, so minimizing fees can make a noticeable difference. The affordability of BND and AGG ensures they remain appealing for those who value cost-conscious investing while working toward their financial goals.

When might an investor choose AGG instead of BND based on liquidity and trading volume?

Investors might lean toward AGG rather than BND if liquidity and trading volume are top priorities. AGG generally sees higher trading volumes, which can translate to improved liquidity. This often means narrower bid-ask spreads, making it simpler and potentially less expensive to execute trades quickly.

For those who trade frequently or need to handle large transactions, AGG's superior liquidity can offer a more seamless experience, particularly during times of market turbulence.

How do BND and AGG react to changing interest rates, and what should investors know about their risk and return potential?

Bond ETFs like BND and AGG are closely tied to interest rate movements. When interest rates climb, bond prices generally decrease, and when rates drop, bond prices usually rise. This inverse connection, known as interest rate risk, plays a significant role in shaping the value of your investment.

For investors, the total return from these funds combines two components: changes in price and the income generated by bond yields. To gauge their risk and return potential, it’s important to consider how factors like duration (a measure of sensitivity to interest rates) and credit quality influence each ETF. Understanding these elements can help you better align your fixed-income strategy with your broader financial objectives.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.