Management fees may seem small, but over time, they can significantly reduce your investment returns. Even a 1-2% fee can cost you thousands in lost growth due to compounding. Here’s what you need to know:

- Types of Fees: Common fees include management expense ratios (MERs), advisory fees, trading commissions, and account maintenance charges.

- Why Fees Matter: A 2% fee on a $100,000 portfolio can reduce your returns by over $200,000 across 30 years at a 7% annual return.

- Calculating Fee Impact: Use the formula:

Final Value = Initial Investment × (1 + Annual Return - Annual Fee)^Years

This helps compare portfolio growth with and without fees. - Reducing Fees: Opt for low-cost index funds or ETFs, consolidate accounts to avoid duplicate fees, and monitor expenses regularly. Tools like Mezzi can help identify and lower fees.

What Is The True Cost of a 1% AUM Investment Fee?

How to Calculate Management Fee Impact Over Time

To understand how management fees affect your portfolio, compare its value with and without those fees applied.

Step-by-Step Fee Impact Calculation

The compound growth formula simplifies this process:

Final Value = Initial Investment × (1 + Annual Return - Annual Fee)^Number of Years

Let’s break it down with an example. Say you invest $100,000 in a portfolio earning a 7% annual return. If a 1.5% management fee is applied, your net return drops to 5.5%. After 20 years, your portfolio would grow to about $292,526. Without the fee, however, the same $100,000 would grow to $386,968 at the full 7% return.

That 1.5% fee ends up costing you $94,442 over two decades. This loss isn’t just from the yearly reduction in returns - it also reflects missed compounding growth over time.

To see the effect year by year, consider this: the 1.5% fee starts at $1,500 in the first year and grows to $4,388 by year 20 as your portfolio increases in value. This step-by-step approach helps you evaluate and compare various fee scenarios effectively.

Fee Comparison Tables and Examples

Now, let’s compare how different fee levels impact your portfolio. Using a $100,000 initial investment with a 7% gross return over 20 years, here’s how three common fee levels - 0.25%, 0.75%, and 1.5% - affect your results:

| Fee Level | Net Annual Return | Portfolio Value After 20 Years | Total Fees Paid | Lost Growth |

|---|---|---|---|---|

| 0.25% | 6.75% | $372,204 | $18,593 | $14,764 |

| 0.75% | 6.25% | $340,870 | $51,087 | $46,098 |

| 1.50% | 5.50% | $292,526 | $94,442 | $94,442 |

The gap between the lowest and highest fee scenarios is staggering - nearly $80,000 over 20 years. The table highlights both the total fees paid and the lost growth - the additional money your portfolio could have earned if those fees had stayed invested.

The longer the time frame, the more dramatic the difference becomes. For example, over 30 years, a $100,000 investment grows to $661,437 with 0.25% fees but only $504,020 with 1.5% fees. That’s a $157,417 difference.

The impact is even greater with regular contributions. If you add $500 monthly to your portfolio over 20 years, the difference between 0.25% and 1.5% fees exceeds $120,000.

How to Research and Compare Management Fees

Understanding how to locate and analyze fee information is crucial for managing your investments effectively. Yet, this remains a challenge for many. Nearly 73% of investors either don't know how much they're paying in investment-related fees or believe they aren't paying any fees at all. Even more troubling, almost two-thirds of investors are unsure where to find this information. Let’s break down where to look and how to interpret the details.

Finding and Reading Fee Disclosures

To uncover fee details, start with the following key documents and resources:

- Account agreements: Look for sections titled "Fee Schedule", "Account Charges", or "Investment Costs." These sections outline the costs associated with your account and investments.

- Account statements: These documents provide a record of fees you've actually paid, such as "Advisory Fee", "Management Fee", or "Account Maintenance Fee." They give a clear picture of ongoing costs rather than just potential charges.

- Trade confirmations: These are useful for tracking transaction-specific costs, such as trading fees.

- Investment company websites: For mutual funds and ETFs, management fees are often listed as expense ratios in the fund's fact sheet or prospectus summary. Look for terms like "Net Expense Ratio" or "Total Annual Operating Expenses".

- Form CRS (Customer Relationship Summary): If you're working with a brokerage firm, this document provides an overview of principal fees for new customers. It often includes hyperlinks to detailed fee schedules available on the firm's website.

By gathering information from these sources, you’ll have a clearer understanding of the fees tied to your investments.

Creating Fee Comparison Tables

Once you’ve identified the fees, organizing them into a comparison table can help you evaluate and manage costs more effectively. This approach allows you to directly assess how fees impact your portfolio and make decisions to minimize unnecessary expenses.

For mutual funds and ETFs, focus on the expense ratio, which includes management fees and other operating costs. For managed accounts, pay attention to advisory fees, typically expressed as a percentage of assets under management. Ensure your comparison includes both direct fees (like management or advisory fees) and indirect costs (such as trading or account maintenance fees).

To simplify the process, use tools like FINRA's Fund Analyzer, which lets you compare the costs of various mutual funds and ETFs. This free resource can show how fees affect your returns over time and across different investment amounts.

Additionally, ask your investment professional about their compensation model and any associated costs. Some advisors earn commissions on the products they sell, while others charge fees based on assets under management. Understanding these details helps you identify potential conflicts of interest and calculate the total cost of your investments.

sbb-itb-e429e5c

Using Mezzi for Fee Analysis and Optimization

Keeping track of investment fees manually can feel overwhelming, but Mezzi simplifies the process by consolidating your investment data and offering actionable insights to help you save money. By turning complex fee information into clear recommendations, Mezzi could save you thousands of dollars over time.

Account Aggregation and Fee Analysis

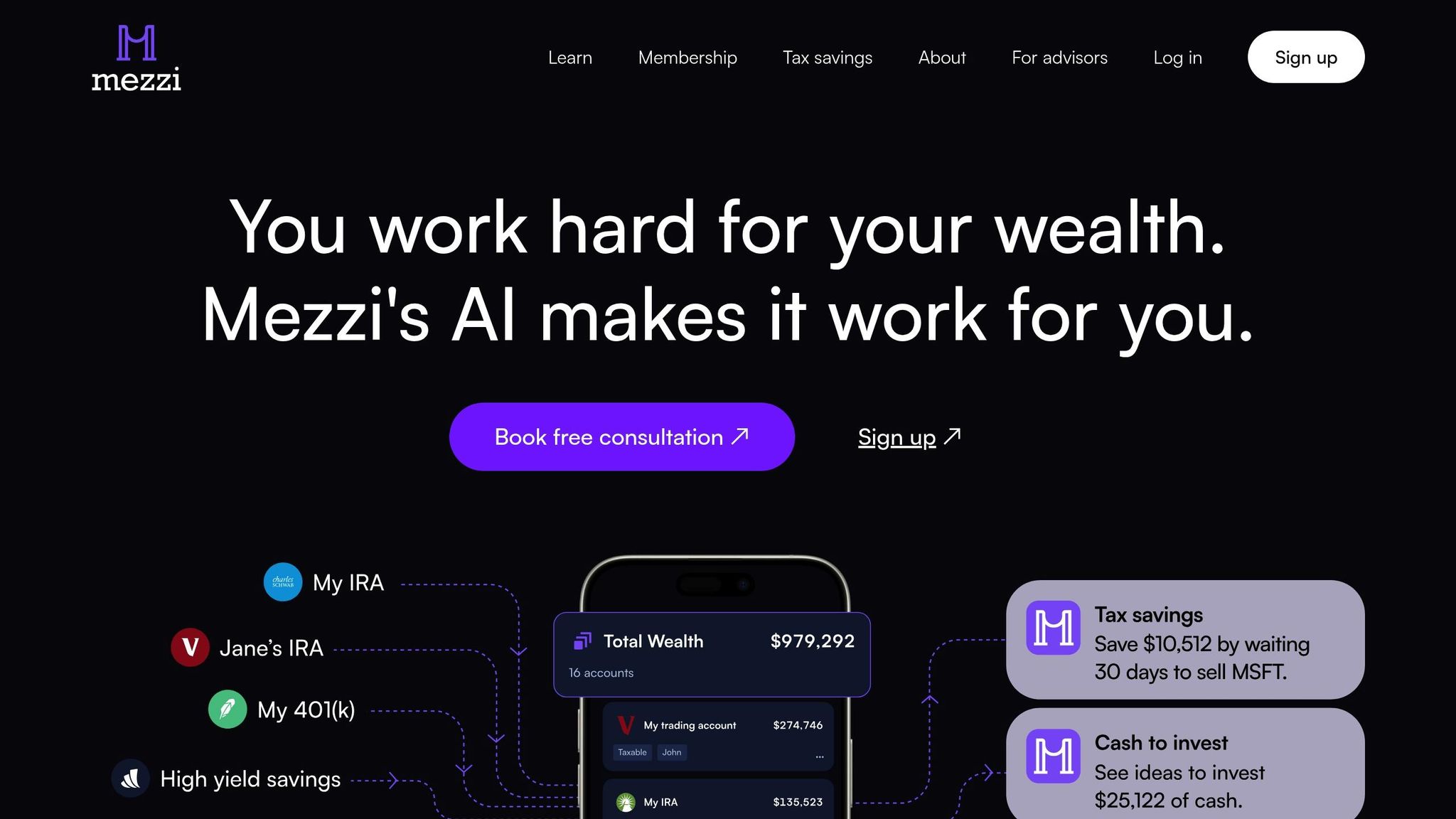

Mezzi uses secure technology to connect with multiple financial institutions, bringing all your investment data - whether it’s from your 401(k), IRA, taxable brokerage accounts, or other holdings - into one easy-to-navigate dashboard. No more hopping between platforms just to figure out what you're paying in fees.

The platform identifies fees that affect your returns, such as mutual fund expense ratios, advisory fees, transaction costs, and other charges like sales loads or redemption fees. By breaking these costs down by account and investment product, Mezzi helps you uncover both obvious and hidden fees that could chip away at your long-term gains.

For instance, if your investments are spread across different accounts, Mezzi might reveal that your 401(k) management fees are 0.75%, your IRA funds have expense ratios ranging from 0.05% to 1.2%, and your taxable account includes 1% in annual advisory fees. With this comprehensive fee breakdown, you can easily pinpoint which accounts or funds are costing you the most, setting the stage for smarter portfolio decisions.

AI-Powered Fee Optimization Recommendations

Mezzi’s AI takes a deep dive into your portfolio, comparing your current investments to similar, lower-cost alternatives. It highlights high-fee options and suggests specific replacements. For example, if you’re holding an actively managed mutual fund with a 1.5% expense ratio, Mezzi might recommend a comparable index fund with a 0.05% fee, showing you how much you could save over time.

The AI doesn’t just focus on cutting costs - it also considers performance, risk-adjusted returns, and tax efficiency. This ensures you maintain or even improve the quality of your investments while reducing unnecessary expenses.

Fee Impact Projections with the Financial Calculator

Mezzi’s Financial Calculator makes it easy to see how fees impact your future wealth. By entering details like your portfolio size, expected annual return, fee percentages, and investment timeline, you can compare projections with and without fees.

The results can be eye-opening. For example, a $10,000 investment with a 2% fee over 10 years (assuming a 10% gross return) grows to $20,446.20, compared to $25,937.42 without fees - a difference of more than $5,000. For retirement planning, even a small reduction in fees - like 0.5% - can translate into thousands of dollars in additional returns.

Mezzi also provides step-by-step guidance to help you act on its recommendations. This includes suggesting alternative funds, outlining transfer instructions, and explaining potential tax implications. As you make changes, you can track your progress and see updated projections, giving you the flexibility to adjust your strategy in real time.

How to Reduce Management Fee Impact on Your Portfolio

Once you've assessed how fees affect your investments, it's time to take action. Here are three practical strategies to help you hold on to more of your returns. Even small reductions in fees can add up to significant savings over time.

Choose Lower-Cost Investment Products

One of the simplest ways to cut fees is by shifting from high-cost actively managed funds to low-cost index funds and ETFs. Actively managed mutual funds often carry expense ratios between 0.75% and 1.5%, while index funds typically charge much lower fees - ranging from 0.03% to 0.20%.

For example, a $50,000 investment in an actively managed fund with a 1.2% expense ratio would cost you $600 annually in fees. Compare that to an index fund with a 0.05% expense ratio, which would cost just $25 per year. That’s a $575 annual savings.

Look for established funds with low expense ratios. Vanguard's Total Stock Market Index Fund (VTSAX) charges only 0.04%, and Fidelity offers zero-fee options like FZROX (Total Market Index Fund) with a 0.00% expense ratio.

If you participate in a 401(k) plan, review the available funds and select the ones with the lowest fees that align with your investment goals. If your plan only offers high-cost options, contribute enough to take full advantage of any employer match, then consider opening an IRA for additional contributions. IRAs often provide access to a wider range of low-cost funds.

Consolidate Accounts to Reduce Fees

Having multiple investment accounts across various firms can mean paying overlapping fees. Each account may come with its own advisory fees, transaction costs, and maintenance charges, which can chip away at your returns.

"Every account you have at a different firm accrues its own set of fees and expenses – both from the firm (like advisory and transaction fees) and from individual investments (like trading fees and expense ratios). This can ultimately represent a drain on your investment returns. When you consolidate your accounts, you can potentially reduce these costs and allow a greater portion of capital to work in your favor." - Derek Pease, Baird Wealth

Consolidating accounts can save you money. Many brokerages waive maintenance fees or offer lower rates when your combined assets exceed certain thresholds, such as $10,000, $25,000, or $100,000. You might also gain access to premium services or institutional-class funds with even lower expense ratios.

Before consolidating, compare the fee structures of your current accounts with those of your target account. Some 401(k) plans offer institutional funds with exceptionally low fees, which could make it worth keeping those accounts separate. In these cases, prioritize contributions to the low-cost plan.

Also, watch out for potential costs of consolidation, such as account closure fees or penalties for early withdrawals. Calculate whether the long-term savings outweigh these one-time expenses before making a move.

Track and Optimize Fees with Mezzi

After consolidating your accounts, keeping track of fees becomes essential. This is where tools like Mezzi can make a big difference. Mezzi aggregates all your investment data and monitors fee changes across your portfolio.

The platform uses AI-driven analysis to find opportunities for savings. It identifies lower-cost alternatives to your current holdings and calculates how much you could save by switching. For example, if you own multiple overlapping funds with varying fees, Mezzi might recommend consolidating into a single, broader index fund that provides the same market exposure at a lower cost.

Mezzi also keeps you updated on changes. If a fund you own raises its fees or a new low-cost option becomes available, you’ll receive alerts and recommendations. The platform’s Financial Calculator models different fee scenarios, showing how much more wealth you could accumulate by reducing fees by 0.25%, 0.50%, or 1.00%.

This ongoing approach ensures your portfolio remains cost-efficient over time. As your investments grow and market conditions evolve, Mezzi adapts its recommendations to help you stay on track while minimizing fees.

Take Control of Management Fees to Maximize Returns

Reducing fees is one of the simplest ways to grow your wealth over time. Even small differences in fees can have a huge impact on your investment returns thanks to the power of compounding.

Start by calculating the total fees you’re paying. This includes expense ratios, advisory fees, and account maintenance charges across your portfolio. Many investors underestimate how much these costs can chip away at their growth potential. Once you see the full picture, you’ll be ready to take action.

Now’s the time to make changes. Review your investments and accounts for any avoidable fees and make adjustments where necessary. Even small reductions can translate into significant savings over the long haul.

To make fee management easier, consider leveraging technology. Platforms like Mezzi use AI to monitor fees, highlight savings opportunities, and project how those changes can benefit you in the future. This allows you to make smarter, more cost-effective decisions.

Fee structures and investment options are always changing, so regular reviews are essential. By staying on top of your fees with tools like Mezzi, you can ensure your portfolio remains efficient, focused on growth, and aligned with your financial goals.

FAQs

How can I identify which fees are reducing my investment returns the most?

When evaluating which fees are cutting into your investment returns, start by looking at the expense ratios of your funds. These annual charges directly chip away at your earnings and can accumulate substantially over time. Beyond that, keep an eye on additional costs like advisory fees, broker commissions, and sales loads, as these can further diminish your overall returns.

To get a clearer picture of the long-term impact, consider using tools or calculators that illustrate how fees can influence your portfolio's growth over time. It's worth noting that higher fees don’t necessarily translate to better performance, so trimming unnecessary expenses can be a smart way to boost your investment results.

What are the best ways to reduce management fees while maintaining strong investment performance?

Reducing management fees while maintaining strong investment performance is achievable with a few smart approaches. One effective strategy is to look into low-cost options like index funds or ETFs. These typically come with expense ratios under 0.05%, which is significantly less than what you’d pay for actively managed funds, all while offering broad market exposure.

Another option is to negotiate fees with your financial advisor or fund manager. Some fees can be adjusted, so it’s worth having that conversation. You might also explore performance-based fee structures, where the fees depend on the manager meeting specific performance benchmarks. This setup aligns their goals with your success, ensuring their focus remains on delivering results.

By staying informed and taking an active role in managing costs, you can prevent fees from chipping away at your long-term investment growth.

How can I use Mezzi to reduce investment fees and boost my portfolio's performance?

Mezzi's AI-powered tools simplify the process of analyzing and cutting down on investment fees, helping you grow your portfolio more effectively. With features like tax-efficient rebalancing and diversification analysis, Mezzi identifies opportunities to save on costs, reduce transaction expenses, and refine your tax strategies. These adjustments can make a noticeable difference in your long-term returns.

To fully benefit from Mezzi, take time to regularly review your portfolio's fee structure. Explore options such as switching to low-cost index funds or ETFs to trim expenses. Even small reductions in management fees can add up significantly over time, thanks to compounding. By tapping into Mezzi's insights, you can take charge of your financial planning and make smarter, data-backed investment decisions.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.