When you invest, taxes can quietly erode your returns. Ignoring tax planning often leads to missed savings opportunities and unexpected liabilities. The solution? Integrate tax strategies into your investment decisions. Here's the key takeaway:

- Track the right data: Cost basis, realized/unrealized gains, dividend/interest income, RMDs, and asset location.

- Streamline workflows: Align account setup, rebalancing, tax-loss harvesting, and year-end planning.

- Optimize asset placement: Use tax-advantaged accounts for tax-inefficient assets and taxable accounts for tax-efficient ones.

- Automate monitoring: Spot wash sales, tax-saving opportunities, and portfolio imbalances in real-time.

Platforms like Mezzi simplify this process by consolidating accounts, automating tax optimization, and offering actionable insights. The result? Better after-tax returns and less stress managing your finances.

Keep reading to learn how to implement these strategies step by step.

WEBINAR: How to Best Integrate Tax Planning Into Your Financial Planning Process

Understanding Data and Workflow Requirements

To build a tax-aware investment strategy, you need accurate financial data and efficient workflows that connect tax planning with your investment activities. It all starts with identifying the information you need to track and understanding how your processes interact throughout the year. From there, pinpoint the key data points that power these workflows.

Key Data to Track

Cost basis and tax lot information are at the heart of tax-aware investing. Each time you purchase shares, you create a tax lot with a specific cost basis and purchase date. When you sell, the IRS requires you to report which shares were sold and their original cost. This can get tricky if you’ve made multiple purchases of the same security over time.

While brokerage statements include tax lot details, many investors overlook this data until tax season. Monitoring realized and unrealized gains and losses year-round is essential. Realized gains happen when you sell an investment, while unrealized gains reflect the value of investments you still hold. Keeping tabs on both allows you to strategically decide when to harvest losses or realize gains.

You’ll also need to track dividend and interest income, as these directly impact your tax bill. Qualified dividends from U.S. corporations are taxed at lower rates, while non-qualified dividends are treated as ordinary income. Interest income varies: municipal bond interest is often tax-free federally, but corporate bond interest is fully taxable.

For those aged 73 and older, required minimum distributions (RMDs) become a critical consideration. The IRS mandates withdrawals from traditional IRAs and 401(k)s based on your account balance and life expectancy. Missing an RMD can result in a steep penalty - 50% of the amount you were supposed to withdraw. Planning ahead can help reduce the tax burden of these distributions.

Finally, understanding asset location data is crucial for optimizing your portfolio. Investments like REITs, high-yield bonds, and actively managed funds generate more taxable income and may be better suited for tax-deferred accounts. Meanwhile, tax-efficient investments like index funds or individual stocks often perform better in taxable accounts, where you can take advantage of lower capital gains rates and tax-loss harvesting opportunities.

Mapping Workflow Touchpoints

Your workflows should align with your tax and investment goals, starting with account setup and funding. When opening new accounts, ensure they fit into your overall financial strategy. Many investors miss opportunities by failing to coordinate account types and investment choices from the beginning.

During regular investment and rebalancing, focus on using tax-advantaged accounts for trades to limit taxable events while keeping your portfolio aligned with your goals.

Tax-loss harvesting requires constant vigilance due to the wash sale rule, which prevents you from claiming a loss if you repurchase identical securities within 30 days, even across different accounts.

As the year winds down, year-end planning becomes critical. This involves reviewing realized gains and losses, finalizing tax-loss harvesting, evaluating Roth conversions, and maximizing contributions to tax-advantaged accounts before December 31.

Finally, tax filing preparation ties everything together. Forms like 1099-B (sales transactions), 1099-DIV (dividends), and 1099-INT (interest income) need to be reconciled with your records to ensure accuracy and catch any discrepancies.

Consolidating Multi-Account Data

Managing multiple investment accounts adds another layer of complexity. Cross-account visibility is essential, especially since the wash sale rule applies across all accounts, even those held at different brokerages. Consolidating your data helps you avoid costly mistakes during tax-loss harvesting.

Tracking asset allocation across accounts can improve tax efficiency. For example, holding bonds in tax-deferred accounts and stocks in taxable accounts can reduce your annual tax burden.

Coordinating contributions and distributions across accounts is also key. For instance, contributing to a traditional IRA might lower your taxable income, creating opportunities for Roth conversions at favorable tax rates. Similarly, HSA contributions provide immediate tax deductions and tax-free growth for retirement expenses.

Evaluating after-tax performance gives you a clearer picture of how your portfolio is performing. A taxable account with strong returns might lose its appeal once you factor in taxes on dividends and realized gains, whereas tax-deferred accounts grow without annual tax interruptions.

Finally, managing cash flow across accounts ensures you’re making the most of your contributions and withdrawals. For example, funding a Roth IRA early in the year maximizes growth potential, while timing traditional IRA contributions based on your projected tax bracket requires careful cash flow planning.

As your portfolio grows, managing this data can become overwhelming. While spreadsheets are a common starting point, manual tracking often leads to errors and inefficiencies. The solution lies in scalable systems that maintain accuracy and provide actionable insights, enabling you to make informed, tax-aware decisions with confidence.

Connecting Systems and Standardizing Processes

After identifying the data you need to track and understanding how your workflows interact, the next step is integrating your investment accounts, tax planning tools, and financial systems. This integration minimizes manual data entry, reduces errors, and ensures your tax and investment strategies align seamlessly.

Linking Accounts and Tools

The backbone of an integrated system is account aggregation. Whenever possible, use direct API connections to access accurate, real-time data. If APIs aren’t an option, manual uploads can serve as a fallback, but be cautious with screen scraping - it can miss transactions or cause delays in updates.

It’s also essential to standardize data across custodians. For instance, Charles Schwab might classify a dividend reinvestment differently than Fidelity, which could disrupt your tax calculations. Look for systems that can normalize transaction types and security identifiers across all accounts to avoid discrepancies.

Your integration system should also handle corporate actions efficiently. Events like stock splits, mergers, or spin-offs can complicate cost basis tracking, particularly when multiple accounts are involved. Automating these processes ensures accuracy.

Real-time updates are critical, especially during periods of active trading or at year-end. For example, if you’re harvesting losses in December, you need immediate visibility into wash sale implications across all accounts. Delays in data can lead to costly errors that only come to light when tax forms arrive.

Standardizing Tax Planning Workflows

With seamless data integration in place, the next step is to standardize your tax workflows for consistency and efficiency. These workflows should be scalable and dependable, whether you’re managing a modest portfolio or a multi-million-dollar one.

- Conduct monthly reconciliations to identify and address discrepancies early, before they escalate into larger issues.

- Perform quarterly reviews to assess year-to-date realized gains and losses, explore tax-loss harvesting opportunities, and project your tax liability.

- Create structured year-end workflows, starting in November with preliminary tax projections and running through January 31 for finalizing tax documents.

Establishing documentation standards is equally important. For every decision - whether it’s harvesting a loss or executing a Roth conversion - record the tax implications and strategic reasoning. This not only creates an audit trail but also provides insights for future decisions.

Be prepared for exceptions. For example, if your aggregation system goes offline during a critical trading period, have backup processes in place to maintain your timeline and avoid disruptions.

Working with Key Stakeholders

To streamline decision-making, integrate key stakeholders - such as CPAs, financial advisors, and family members - into your unified data system.

Your CPA or tax preparer should have access to accurate investment data well before tax season. Set up quarterly data-sharing practices to keep them informed about significant transactions and planning opportunities.

For more complex situations involving trusts, multiple entities, or business interests, use shared workspaces for secure, direct access to data. This simplifies collaboration and reduces the risk of miscommunication.

In households with multiple investment accounts, family coordination becomes crucial. Shared visibility into relevant account data helps align decisions on charitable giving, education funding, and estate planning.

Finally, establish clear communication protocols to define who is responsible for making decisions and when. For instance, if your tax professional identifies a Roth conversion opportunity, ensure there’s a clear process for coordinating with investment accounts to complete the transaction. This avoids delays and ensures no opportunities are missed.

Implementing Tax-Aware Portfolio Strategies

By leveraging integrated tools and following standardized workflows, you can align investment decisions with tax planning to improve returns while managing tax obligations. These strategies require precision and coordination, making the right tools essential for success.

Tax-Loss Harvesting

Tax-loss harvesting allows you to offset taxable gains by selling securities at a loss across various accounts. However, the wash sale rule prevents you from claiming a loss if you repurchase a substantially identical security within 30 days.

Direct indexing - owning individual stocks instead of an ETF - can create more opportunities for harvesting losses while keeping your market exposure intact. For instance, if you hold individual stocks from the S&P 500, you could sell underperforming tech stocks to realize losses while maintaining your overall allocation.

Timing is critical here. Harvesting losses in December can be especially effective. For example, realizing $10,000 in losses by December 31 can offset $10,000 in gains, eliminating your capital gains tax liability for that amount.

To avoid triggering a wash sale, consider asset substitution. If you sell Apple stock, for example, you could replace it with a similar technology ETF or individual stocks to maintain exposure without violating the rule.

State tax differences also play a role. Some states don’t tax capital gains, while others have rates exceeding 13%. If you’re planning to move from California to Texas, timing your gain realization around this move could save you thousands in state taxes.

Next, let’s look at how to strategically position your assets for maximum tax efficiency.

Asset Location Optimization

Asset location involves placing specific investments in the most tax-advantaged accounts. This approach complements the broader system you've established.

- Tax-inefficient assets like REITs, high-yield bonds, and actively managed funds that generate significant taxable distributions should go into tax-deferred accounts (e.g., 401(k)s or traditional IRAs). For example, holding a REIT yielding 8% in a taxable account could cost 2.56% annually in taxes if you're in a 32% tax bracket.

- Tax-efficient assets - like low-turnover index funds, stocks held long-term, or municipal bonds for high earners - are better suited for taxable accounts. These investments generate minimal taxable income and can benefit from a step-up in basis at death, potentially eliminating capital gains taxes for your heirs.

- Roth accounts are ideal for high-growth investments. Since Roth withdrawals are tax-free, you’ll want to place assets with significant growth potential - like small-cap stocks or emerging market funds - in these accounts to maximize their tax shelter.

If you’re investing across multiple account types, asset location becomes more complex. For instance, if you have $100,000 split between a taxable account, traditional IRA, and Roth IRA, you might allocate bonds to the traditional IRA, high-growth stocks to the Roth IRA, and index funds to the taxable account.

Rebalancing also requires careful planning. Instead of selling appreciated assets in a taxable account, you can direct new contributions to underweighted asset classes or rebalance within tax-advantaged accounts to avoid triggering taxable events.

Timing Contributions and Distributions

The timing of your contributions and distributions can further sharpen your tax strategy. Aligning your investment timeline with tax deadlines and market conditions is key.

- Front-load 401(k) contributions early in the year to maximize tax-deferred growth. For example, if you receive a bonus in March, contributing the maximum amount immediately allows more time for compounding.

- Roth conversion timing is another critical factor. Converting traditional IRA assets to Roth during low-income years - such as early retirement - can reduce the tax cost. For instance, if your income drops from $80,000 to $40,000 during a job transition, converting assets to fill lower tax brackets can be highly effective.

- Required minimum distributions (RMDs), which begin at age 73, also require coordination. Taking them early in the year can provide flexibility for tax-loss harvesting, while delaying until December allows you to assess your income for the year. If you don’t need the funds, consider qualified charitable distributions from your IRA to satisfy the requirement without increasing taxable income.

Charitable giving offers additional tax advantages. Donating appreciated securities instead of cash avoids capital gains taxes while allowing you to deduct the full market value. Using a donor-advised fund, you can bunch several years’ worth of contributions into one tax year to exceed the standard deduction threshold.

Coordinating tax-loss harvesting with contribution timing can also reduce your tax burden. For example, if you plan a large Roth conversion that increases your tax liability, harvesting losses earlier in the year can offset some of that cost. Similarly, timing the exercise of stock options alongside available losses can minimize taxes.

Lastly, high earners should consider the Medicare surtax and net investment income tax. These taxes apply when your modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly). Managing income recognition and loss harvesting around these thresholds can save 3.8% on investment income and an additional 0.9% on earned income.

sbb-itb-e429e5c

Automating Monitoring and Reviews

Once you've implemented tax-aware portfolio strategies, keeping a close eye on them is essential. Managing multiple accounts, navigating complex tax rules, and responding to shifting market conditions can quickly overwhelm manual processes. That's where automation steps in to keep your strategies on track while minimizing compliance risks.

Setting Up Alerts and Monitoring

The first step in automation is identifying the events that need your immediate attention. For example, wash sale monitoring is a critical area to automate. The wash sale rule applies to transactions within a specific timeframe around a sale, so it's vital to have systems that track purchases across all accounts and flag potential issues before they arise.

Another smart alert to set up is for securities that drop significantly below their cost basis. If a stock's price dips to a level that creates a potential loss harvesting opportunity, an automated alert can prompt you to evaluate whether selling aligns with your overall tax strategy.

Automated systems can also help maintain your portfolio's balance by sending asset allocation alerts. These systems monitor holding periods to ensure you qualify for long-term capital gains treatment. Additionally, they can track retirement account contribution limits and notify you when your income approaches thresholds that might trigger extra taxes, enabling proactive adjustments to your tax planning.

All these alerts feed into regular reviews, ensuring your strategies stay aligned with your goals.

Conducting Periodic Reviews

With real-time alerts in place, it's important to schedule regular reviews to evaluate your tax strategy's performance. Quarterly reviews, for instance, can focus on performance attribution to confirm whether your tax strategies are delivering the expected savings.

Compare your realized tax savings against your projections and investigate any gaps. If savings fall short, look into factors like transaction timing or missed loss harvesting chances. This type of analysis helps fine-tune your strategy for future success.

Periodic reviews also give you a chance to assess the overall effectiveness of your tax-investment framework. Examine how well your loss harvesting, asset location, and other strategies are contributing to your after-tax returns. Be sure to account for any changes in state tax laws, especially if you've moved or if local regulations have shifted.

Ensuring Security and Audit Readiness

Automated systems must prioritize security and maintain a robust audit trail to ensure compliance. Every data interaction should be logged to create a clear record.

Protect your data with encryption, both in transit and at rest, and implement multi-factor authentication for an added layer of security. Regular security audits are also essential to keep your systems up to date with the latest standards.

Set up routine backups to safeguard historical data and follow recommended record-keeping practices to meet regulatory requirements. For significant transactions, incorporate approval workflows that require confirmation before execution. This extra step reduces the risk of costly mistakes and adds a layer of oversight. Keep detailed documentation for all tax-related transactions to simplify tax preparation and support future audits.

Lastly, ensure your automated systems are updated regularly to reflect any changes in tax laws or regulations. Keeping your systems compliant is vital to maintaining the seamless integration of your tax and investment strategies over the long term.

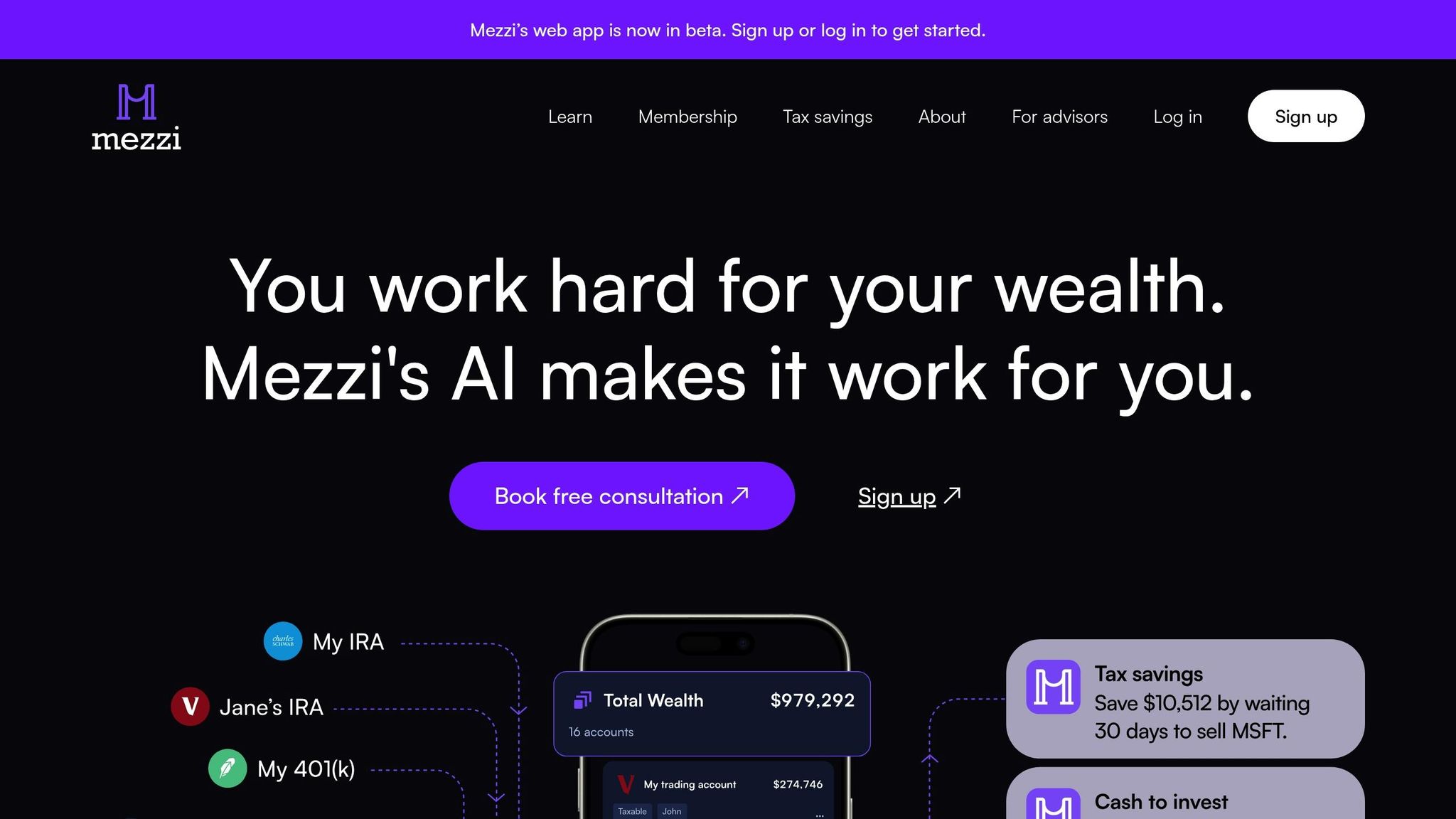

How Mezzi Facilitates Tax-Investment Connection

As we’ve discussed earlier, having precise data and seamless integration is critical for effective tax planning. Trying to manually align tax strategies across multiple accounts can quickly become overwhelming. That’s where Mezzi steps in. This advanced platform simplifies tax-aware portfolio management for self-directed investors, giving them access to tools that were once exclusive to high-end financial advisors.

Let’s dive into how Mezzi’s unified account view can streamline your tax strategy.

Unified Account View

Managing tax strategies across scattered investment accounts often leads to blind spots, which can result in missed opportunities or even compliance issues. Mezzi tackles this problem by combining all your financial accounts into one centralized dashboard, enabling a true cross-account analysis.

But this isn’t just basic account aggregation. Mezzi provides a complete financial snapshot in a single, intuitive view. This level of consolidation is crucial for spotting intricate tax scenarios that might span multiple accounts.

For example, if you’re considering tax-loss harvesting in a taxable brokerage account, Mezzi can simultaneously check your IRA and 401(k) to ensure you don’t accidentally violate the wash sale rule by purchasing similar securities elsewhere. This integrated approach also helps with precise asset location, suggesting where to hold specific investments based on their tax implications.

With this solid foundation, Mezzi’s advanced analytics take your tax strategy to the next level.

Advanced Tax Optimization

Mezzi’s AI-powered tax optimization goes far beyond basic portfolio tracking. The platform actively monitors all your accounts to prevent wash sales and flags tax-saving opportunities in real time, reducing the risk of costly manual errors.

For instance, Mezzi can identify securities trading below their cost basis that could be ideal for tax-loss harvesting. At the same time, it ensures that any harvesting aligns with your broader investment goals. This isn’t just about saving on taxes - it’s about keeping your portfolio on track for long-term success.

One standout feature, the X-Ray tool, identifies hidden portfolio exposures you might not even realize exist. This is especially valuable for tax planning, as it helps uncover overlapping positions across accounts that could complicate loss harvesting or lead to unintended concentration risks.

By addressing these challenges proactively, Mezzi sets the stage for meaningful long-term savings.

Efficiency and Long-Term Savings

As we’ve seen, automated monitoring doesn’t just save time - it also boosts after-tax returns. For investors juggling multiple accounts, Mezzi eliminates hours of manual analysis and cross-referencing, making it easier to implement complex tax strategies effectively.

The platform’s Financial Calculator goes a step further by factoring in asset manager fees when projecting retirement outcomes. This helps you understand how fee structures impact your wealth over time and make smarter decisions about account types and investment vehicles from a tax perspective.

In fact, Mezzi estimates that you could save over $1 million in 30 years by avoiding advisor fees, reducing tax errors, and improving after-tax returns.

Through its Premium Membership, Mezzi offers real-time AI prompts and unlimited AI chat capabilities, ensuring you have access to expert-level financial guidance whenever market conditions change or new opportunities arise. Whether it’s year-end tax-loss harvesting or deciding the timing of contributions, Mezzi helps you act quickly and strategically.

Conclusion: Building a Tax-Aware Investment Strategy

Creating a tax-aware investment strategy involves more than just preparing for tax season - it requires a year-round, integrated approach that aligns your accounts, tools, and strategies.

Start by consolidating data across all your accounts and establishing standardized workflows for tasks like tax-loss harvesting, asset location, and cash flow management. By connecting your systems, you not only reduce manual errors but also reveal opportunities across accounts that might otherwise go unnoticed.

Today’s fintech platforms can send real-time tax law updates, shifting your focus from annual tax preparation to continuous planning. Instead of reacting to tax situations after the fact, you can actively manage them throughout the year. For instance, connected systems can help you avoid pitfalls like triggering wash sales in retirement accounts while harvesting losses in taxable accounts. When your tax and investment tools work together seamlessly, you can confidently execute even the most intricate strategies.

Once you’ve built a solid foundation, automation becomes a powerful tool. Use it to monitor tax-loss harvesting opportunities, track asset allocation drift, and stay on top of contribution deadlines. Regular reviews ensure your strategy keeps pace with changing tax laws and market conditions, while also maintaining compliance and audit readiness.

For self-directed investors, platforms like Mezzi simplify the process by eliminating manual cross-referencing and offering advanced strategies that were once only available through high-end advisors. With features like a unified account view, AI-driven tax optimization, and real-time monitoring, these tools become increasingly valuable as your financial situation grows more complex.

The goal is clear: improve after-tax returns through better coordination between tax and investment strategies. Start with centralized data and streamlined processes, then gradually integrate automation and advanced features as your needs evolve.

FAQs

How does combining tax planning with investment tools help increase my after-tax returns?

Combining smart tax strategies with investment tools can significantly boost your after-tax returns. Techniques like tax-loss harvesting, tax-efficient asset allocation, and reducing taxable income allow you to keep more of your earnings while staying compliant with tax regulations.

Platforms such as Mezzi can simplify this process by automating these strategies, saving you time and helping to avoid expensive mistakes. This forward-thinking approach not only ensures your investments are optimized for tax savings but also keeps them aligned with your long-term financial objectives, paving the way for faster wealth growth.

How can I effectively track and manage tax-related data across multiple investment accounts?

To stay on top of tax-related data across multiple investment accounts, having the right tools to bring all your financial details together is key. Platforms like Mezzi allow you to view your accounts in one place, giving you clarity on tax considerations and helping you fine-tune your financial strategies.

Keeping thorough records of every transaction - like purchase dates, amounts, and sales - is vital for accurate tax reporting and staying compliant. On top of that, using tax-aware investment tools can help you minimize avoidable tax hits, such as wash sales, and take full advantage of tax-saving opportunities available to you.

What is the wash sale rule, and how can I avoid it when using tax-loss harvesting?

The wash sale rule is designed to stop you from claiming a tax loss on a security if you purchase the same or a substantially identical one within 30 days before or after selling it at a loss. This can throw a wrench into your tax-loss harvesting strategy if you're not careful.

To navigate this rule effectively:

- Wait 31 days before buying back the same security you sold at a loss.

- Choose a similar, but not identical, investment to keep your portfolio aligned while staying within the rule's boundaries.

By sticking to these approaches, you can manage losses strategically and keep your tax planning on track without violating the wash sale rule.

Related Blog Posts

Table of Contents

Book Free Consultation

Walk through Mezzi with our team, review your current situation, and ask any questions you may have.